💵 How ACH Works

💵 How ACH Works

What are ACH Payments?

An automated clearing house (ACH) is a computer-based electronic network for processing transactions, usually domestic low value payments, between participating U.S. financial institutions. It may support both credit transfers and direct debits. The ACH system is designed to process batches of payments containing numerous transactions, and it charges fees low enough to encourage its use for low value payments.

Supported Countries

ACH processing is only available in United States of America (all 50 states)

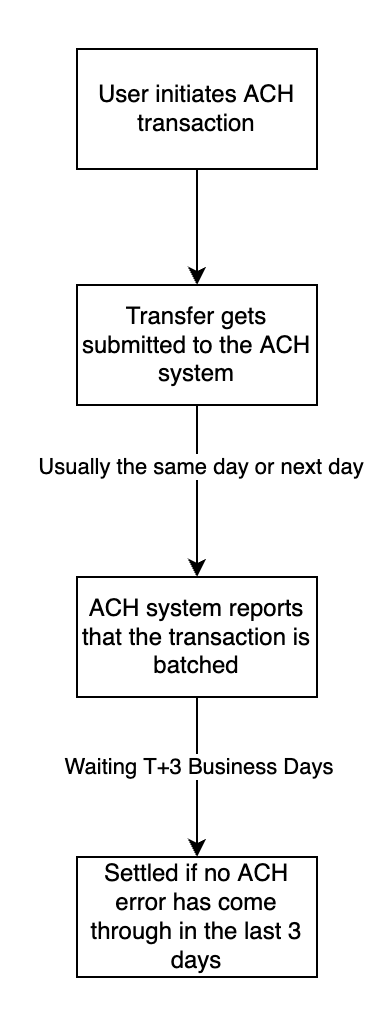

How ACH works

ACH payments go through several status updates as it makes its way along the pipeline to be authorized and processed by the networks. The following statuses indicate where an ACH purchase is in the process:

When do ACH payments settle?

ACH payments do not settle for T+3 Business Days after batching. Meaning in the worst case, with a long holiday weekend, someone initiating an ACH payment on Friday afternoon, settlement will not happen until Thursday of the following week. This can cause customer confusion because the purchase is not immediately available in their account at the point of purchase.

🚧 ACH payments takes 3 business days to settle and authorization is not instant.

To avoid fraud, Coinflow does not finalize settlement to the merchant until after the ACH payment has fully cleared.

ACH Payments with Saved Bank Accounts

Bank accounts are stored for users once entered into the system and can be used for purchasing. Users will be able to conveniently make subsequent purchases, improving the system interaction and improving conversion.

Coinflow is PCI-compliant and does not store the bank account data directly on our servers.